The following note was sent out to our advisoryclients in February. This was in response to the jitters, some of them were experiencing after a 15% drop in the market. I think this is valid in all kinds of markets including the optimistic one we have now.

——————————————

I am not feeling any better knowing that the model portfolio is down less than the overall indices. I increased the cash holding a bit in the last few months and avoided the momentum stocks in the later part of 2015. Inspite of these defensive measures, the portfolio is getting hit and it is not pleasant to see losses every day.

At the end of 2014, after a 100%+ rise, I had written the following

It is easy to feel smug and complacent after a 100%+ rise in the portfolio. However it is precisely at this stage that the risks are the highest. The various companies in our portfolio are performing quite well in terms of business performance (topline and profit growth). In addition, we exited a few companies where I felt that the performance depended more on the macro than the company specific condition such as the management or the target market

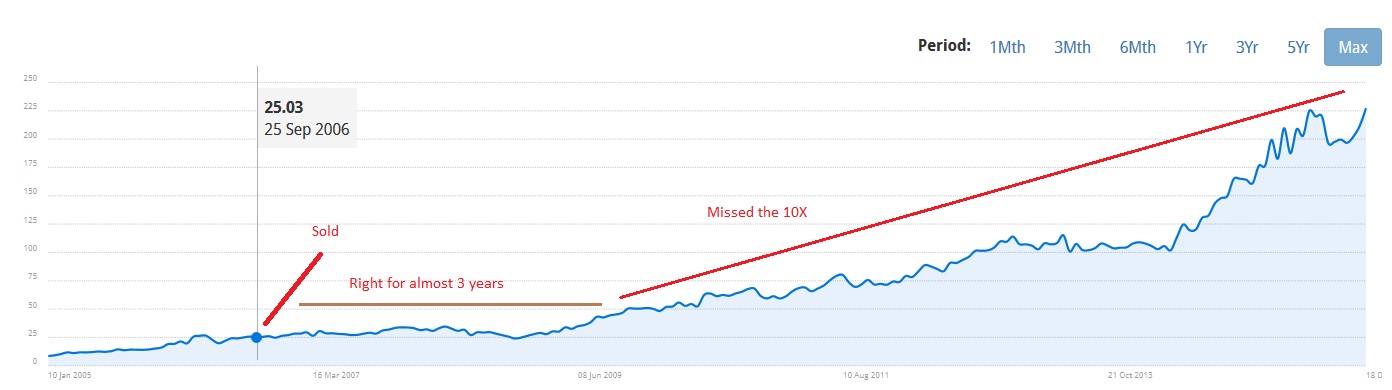

If your time horizon is less than 3 years and you cannot bear a 15%+ drop in the portfolio, then you need to take action when the times are good (such as now) and not after the market drops due to some macro factor.

In my case, I consider my equity investments with 3-5 year perspective (or more) and will continue to hold the positions through any future volatility.

I did not know when a drop in the markets will happen, but was sure that it would occur as that is the nature of markets – greed and fear. We had a period of greed in 2014 and 2015, which has now turned to fear.

The recent events and volatility we are seeing, is not new and has occurred from time to time. The reasons have been different, but the end result is the same – fear and rush to the exits.

At times like these, no one is looking at the company and its fundamentals. The selling is often driven by panic and a desire to reduce the pain.

The only difference is that I try to ignore the pain and focus on the individual companies, their business and the intrinsic value. That helps me in maintaining some level of rationality.

How to handle the volatility

Let me share how I am looking at the current situation (as I have done in the past)

Let’s say (and I hope that is the case), that you have invested your capital with a 2-3 year time horizon. As long as the market is rising, everyone is a long term investor. It is times like now that this belief is tested. There is no dial which increases or reduces the time horizon at an aggregate level. One needs to look at each holding and decide if you will be comfortable holding that position for the next couple of years.

I have been doing that for all the positions in the model portfolio and have exited some, where my level of confidence was not high . As the market crashes and causes some level of business risks, it is important to have a decent understanding of the companies in the portfolio.

Position size and diversification

I have often been asked about position size and the level of diversification one should have in the portfolio. I have a much simpler approach – size it to a point where you can sleep well. If the size of a position or the level of diversification causes you lose sleep, then it is too high.

Look at the intrinsic value

I have always emphasized the important of intrinsic value and its growth for a company. One should always focus on that number. As a long as that number is stable or increasing, then one should stop worrying about the stock price.

Another common feature at a time like this is the tendency of investors to call the bottom of the market. This is a toxic way of managing the portfolio. It leads to a focus on the short term and disappointment if the turn does not happen.

My approach during such times in the past has been to add to my positions slowly over time as they became cheaper (subject to size limits) and not expect to make a killing in the short term.

The final point I have to make is that there is no magic pill for courage. There is a reason why equities have high returns – Volatility and risk.

My effort is to reduce the level of risk (of permanent loss of capital) in the portfolio. I have not tried to reduce volatility actively. Courage and ability to ignore the volatility comes down to temperament and that cannot be supplied by anyone.

– Think long term and focus on the portfolio with a 2-3 year time horizon. This means you should not be investing any money which is needed in less than 3-5 years.

– Ensure that the position size for each stock and the overall diversification lets you sleep soundly at night

– Focus on intrinsic value and performance of each company

– Do not try to time the market (now or any other time)

– Avoid listening to forecaster, pundits and other doom and gloom guys. It will weaken your resolve

– If you manage to hold your nerves and plan to invest, stagger it over time. I am planning to do the same.

—————-

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.