The special situation discussed in the previous post was a delisting announcement by Elantas beck. The plan was to benefit from the price appreciation between the deal announcement and the actual delisting.

A few Comments and some emails on the previous post made me realize that understanding delisting norms is really not everyone’s idea of fun. So let me try to explain it in brief (while omitting some details)

If you hear a thud sound while reading this post, it is likely you have fallen asleep and hit your keyboard while reading this post 🙂

Delisting process

You can find the delisting norms here. In brief, the rules for delisting apply when a company wants to delist all its shares from the exchanges (i.e go private with no public shareholding). It needs to go through a prescribed process which can be described in short as follows

1. Board approves delisting

2. Company seeks shareholder approval for delisting the shares. For the delisting to be successful, the company has to buyback atleast 50% of the publicly held shares. So if the public holding is 11.5 % (as in case of elantas), then the minimum buyback has to be 5.75% of the total shares for the company to delist from the exchange.

3. Shareholders approve the buyback.

4. The company launches reverse book building to discover the price at which it can buy 50% of the outstanding shares. The shareholders tender their shares to the company at their desired price. If the company finds that more than the outstanding number of shares have been tendered and the price for the 50% of the shares tendered is within their target price, then they can declare the offer successful. The company is then obliged to buy all the shares that have been tendered at or below the declared price.

Let’s try to understand this with an example. For simplicity, let look at the case of elantas beck.

Elantas announced a delisting and the share price jumped from 250 levels to around 450 levels in response to it. Finally the company announced on 7-dec, that the board has approved a buyback with a floor price of 219 which is the minimum price based on the delisting norms. In addition the board approved a price of 330 as the offer price. This would be the minimum price paid to the shareholders, if the discovered price turns out to be at or lower than 330 during the reverse book building process.

The price was steady around 470-480 levels and as the reverse book building date approached, it crept upto around 500 levels. Finally after the first two days into the book building process, only .5% of the shares had been tendered and the price in the open market was around 525. As the probability of the success of the offer was low, I exited the stock completely booking around 7-8% gain over the deal.

At the end of the tendering period (around 6-7 days), the company received about 25-30% of the outstanding shares and hence irrespective of the price tendered (which ranged from 210-1100), the offer was not successful (as less than 50% of the shares had been tendered).

About the company

It is not crucial to know about the company in detail in an arbitrage or special situation such as delisting. However when analyzing such a deal, it is important to have a look at the fundamentals of the company and evaluate if the company is overvalued by a large margin at the current price.

Elantas beck is into specialty chemicals for insulation and construction industry. It has performed well in the last few years with an ROE in excess of 20%, zero debt and a 10% growth in bottom line. The company has cash equivalents of around 35 crs which is almost 10% of the market cap. At the time of delisting the company was selling at around 16-17 times earnings which is right around fair value of the company.

If the valuation at the time of the announcement is high, the downside risk of the deal is high if it fails.

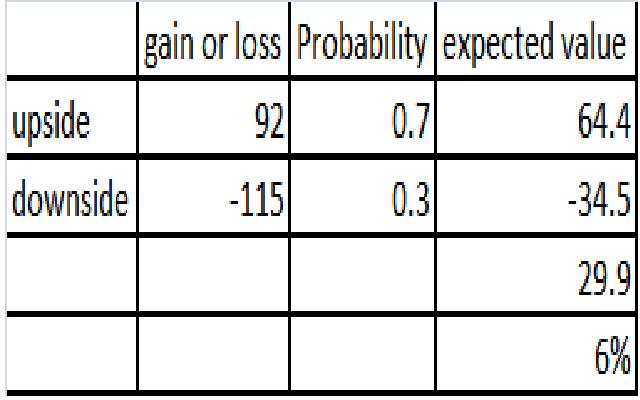

The calculations

The matrix in the previous post is the expected value analysis. The formulae for expected value is gain*probability of gain+loss*probability of loss.

I estimated that the delisting price would be around 580-600 and hence there was an upside of around 100 Rs. On the downside I expected the price to drop to around 360-370 levels and hence a possible loss of around 110-120 Rs. The probability estimates for each of the events was a subjective number and it depends on one’s experience and guess.

All this work for a measly 7%?

The return was around 7% for 1.5 months, which works out to 56% annualized. My return expectations are 20% per annum from arbitrage over the course of the next few years. There will be some deals which will work out well and some where I will lose money. In aggregate i am targeting 20% or more. I don’t expect too much from myself 🙂

The advantage of arbitrage is that the returns are not correlated to market returns. If you can evaluate the deals well, the returns are independent of the market. This helps in reducing the volatility of the portfolio and it is always a better to have an additional tool to invest and make decent returns.