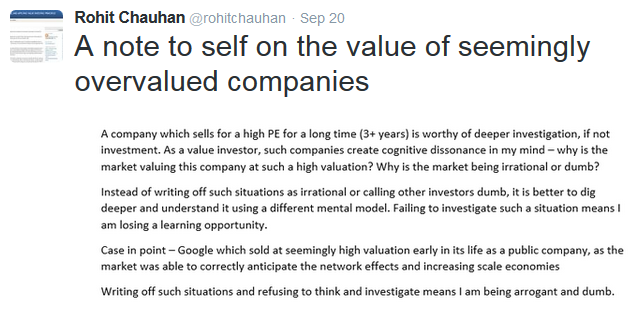

I recently tweeted the following

I have never quite understood the point of these debates. There is obviously no single way of making money in the stock market. There are short term traders, buy and hold guys, debt specialists and all kinds of people in-between. Each approach has its strengths and weaknesses and no one can claim that a specific approach is inherently superior to the other, unless they are equally proficient in both.

The value of learning

Some of you who have followed me on my blog, would have noticed that I try not be a dogmatic about any specific style. I have tried multiple approaches and continue to do so. I do have a dominant style which suits my temperament – buy decent quality companies and hold them for the long run, but I have tried deep value, arbitrage, options and all other types of investing.

A valid question would be – why bother? Why not find an approach which works for you and then just stick with it (and maybe even publicly defend it as your faith 🙂 )

In a similar fashion if you are a deep value investor, what should be your reaction to the success of investors who buy and hold seemingly overvalued stocks?

My counter point – sure that is possible, but what if this bubble has lasted for 10-15 years in some cases. Will you still just wave away these anomalies and label them as flukes?

Why not 5 years? Well now we are moving from the physical to the meta-physical 🙂 and debating the nature of reality.

New business model or value capture

I think the first point to look for is whether there is a change occurring in the business model/ design, wherein due to changing customer needs and priorities, a new type of design is now more suited to meet them more profitably.

For example, a rise in the income levels has caused the retail consumer to now value quality, brand image and convenience in addition to the price. As a result, companies which can meet this new set of needs have been able to create a lot of value.

Example: Cera sanitary ware, Amara raja batteries, Astral polytechnic etc

It is not sufficient to be able to meet the changing needs of the consumer, better than the competition. For starters, the opportunity size should be large so that the company can grow for a long time to come.

An additional point to keep in mind is the need for the company to develop a durable competitive advantage. Let’s take the case of the telecom industry in the early 2000s. The need for communication and mobile telephony was recognized by a few companies such as Airtel in the late 90s and these companies moved in quickly to satisfy the needs.

In such cases seemingly overvalued companies were truly overvalued.

A productive area for finding multibaggers is in the microcap space, where the company operates in a niche and is growing rapidly as its business model is uniquely suited for that niche. In addition, the niche is large enough for the company to grow for a long time, yet not so big that it attracts large companies initially.

A small company develops a unique set of skills for this specific segment and is able to dominate and grow within the segment for a long time. In addition as the niche is quite small, it does not attract much competition till it reaches a certain size.

A lot of these companies appear to be overpriced after they have started growing, but this ignores the possibility of above average growth and a dominant position for the company.

This is a term used by Thomas Russo (see talk here) to describe companies which are capable and willing to make investments in the business for the long term, even though it penalizes the profits in the short term.

Look at the example of Bajaj corp (an old holding which I have since exited). The company acquired no-marks brand in 2013 and started deducting the brand value on their P&L account. In reality the brand value is actually going up as the company continues to spend heavily on advertising (17% of sales) and hence the profits are understated.

Platform Business

This is good note on what is a platform business

The company has since then delivered a return of around 26% p.a and I am sure this qualifies as a great return. So why did a company which appeared so overvalued turn out to be a 10 bagger.

Once this base was built, the company extended it to other platforms such as mobile where the next leg of growth has kicked in. These type of companies also have a very low marginal cost of production and hence any growth beyond a threshold, drops straight to the bottom line.

Such companies have been referred as platform companies and usually appear highly overvalued in the early stages of growth. Another similar company seems to be Facebook.

Rate of change matters

Let me introduce a new concept – business clock speed which I read here. This is the rate at which a business is changing. For example the rate of change in the social media business is high and conversely there are business such as paints or undergarments where the rate of change is low.

On the contrary very few high change businesses (google, Facebook being a few exceptions) turn out to justify their sky high valuations.It is difficult to establish a strong competitive position in an industry where the basis of competition keeps changing every few years – Just look at IBM which has had to re-invent itself almost every decade to stay in business and grow its value. For every IBM, there is DEC or Sun microsystems which did not make it.

It is important to understand at this point that it is quite rare to find overvalued companies, which in hindsight turn out to be undervalued. A lot of overvalued companies, actually turn out to be just that and so it is important for a value minded investor to be cautious about such companies.

So why study ?

As I stated in the beginning of this note – If you want to be a successful investor, it is important to have as many mental models in your head. Investing in a cheap, low valuation companies is one such mental model. However this does not mean one should just wave away any company which is selling at a high price.

– Is the company overvalued simply because the management is investing in the business for the long term which has suppressed the near term profits?

– Is the company developing a new business model which meets the changing requirements of the consumer much better than competition

– Does the company have a durable advantage and a large opportunity space (the case for a lot of FMCG companies in India)

– Does the company have network effects or is it a platform company run by an intelligent fanatic?

– Has the company identified and developed a unique business model for a niche which it will dominate for a long time?

Inspite of the odds, if however if you do manage to get it right, it would be stupid to sell the company based on a PE ratio which appears higher than normal.

—————-

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.

Rohit,Let me be the first to comment – Fantastic post!!Distilled gyaan from multiple models, all woven together neatly in a simple and easy to understand post. This is the reason it is always a pleasure to read your blog and I wish you would blog more often.Coming back to topic, I wonder if you have come across any study which talks about probabilities of capital loss for these various models. I assume it would be different across all these situations and if one understands them well she could apply it for payoff calculations and position sizing as well.e.g. In a platform kind of business with winner takes all, assuming only 1 out of 10 companies succeeding, an investor could expect to lose 70-100% of investment capital in 9 out of 10 cases. This would probably dictate the percentage of portfolio which can be realistically allocated to such ideas while controlling the risk of capital loss. If its a small percentage, even after earning high rate of return it may not matter much at portfolio level compared to a business following a boring model, promising a lower rate of return but with possibilities of much higher allocation possibilities due to higher chances of success (and lower chances of capital loss).mkd

dear rohit,wonderfully expressed all my views in your words. firstly, debate is because when you hold a stock which is overvalued , the price correction is sometims very sharp. then, we look back to see if we did not take advantage of a transient market ineffeciency eg cer correcting by 50%secondly , more painful is how undercvalued is a undervalued comapany and for how long— eg ricoh, fdc, mayur, . here we lose big time.thirdly, do we let go transient but massive mispricing eg textile stocks, mid cap pharma where value was very very obvious.although , a disciple of yours i want to make money always and also be rich. so, i look for all multiples to a 100x( 10×10, 5×20 etc).phelps with multiplication and market cycle churning always helps since it is natural

dear rohit, high PE investing is all about the risk you want to take to prove your hypothesis. if your knowledge advantage mitigates the risk, you are safe. but, as graham pointed out , you are safest when all the three components of an investment indicate safety- industry/ company, your gut, and the market. and high PE fails there.

Brilliant one

Thorough analysis. As WEB says, it's simple but not easy. Happy investing!

Hi Rohit,Just loved your post. Thought you might want to see this on google analysishttps://www.youtube.com/watch?v=VBVEaifDx_A&list=PLGGpadyh0wS53HdovgrEgRwEqHcWrJwgP&index=7 Regards,Sarvdeep

Hi mkdthanks for the comment.I have not looked at the probabilites of each model, as my aim is to first look at some common patterns. also its not easy to find the base rate in each case.i look at each of these models more like a point of view or tool to see where the company is going. for example, a platform company is a type of company with google and facebook being pure example. but we can have companies where they may not be a pure platform business but still have those characteristics.in such cases, even if i dont have the exact probabilities, thinking of the company in that sense will show me that the growth possiblities are much higher and hence a seemingly high valuation is not too high and the business is more fairly priced.so most of these models are more different lens to view a company and not really a precise approach to value itrgdsrohit

hi madhuits comes down if you can play both the approaches well. if you can jump in and out of undervalued positions, all the better. i dont find that easy for me and too much of a headache. buy and hold has worked better for me.does it mean a few % less returns ..sure , but i am happy with what i make 🙂 adding a few extra % and being miserable does not work for me. i feel sick in my stomach literally when i hold crappy companies even if they eventually make money for me. that does not mean it will not work for others

hi anonyou are missing the point. a high PE in an of itself does not mean overvaluation …it could be but not always and that the point of my post.undervaluation in all aspects is a wonderful thing and we had that in 2013, but not now..atleast its not pervasive. so if you can be patient and wait for that kind of situation to come back, then its fine.also graham type of investing does not work as well in india. if you run graham filters most of the time one get horrible biz with bad managements. also overall returns are lower. finally what was a deal breaker for me was that i felt sick in my stomach when i held such lousy companies. so i have realised my temprament does not work for really cheap companies

hi lucky/ chandramouli – thanks for the commentHi sarvdeep – will watch the video ..thanks for sharingrgdsrohit

Hi Rohit,Can we apply the same logic to Mumbai real estate price? It has been almost 8-10 years and the market is expensive. Many believe that there will be a price correction in real estate prices; however it just doesn’t come up.In that case, it is quite possible, that the expensive price is actually the right price and the market is discounting the future growth in infra in Mumbai correctly.I thought that there should be a price correction about 5 years back but it has almost tripled since then.Regards,Swapnil

Hi Rohit,Excellent post. As an investor who started very staunch value guy, I realized over time that such “rigidity” does not help at all. One should be flexible in at least understanding various models that works and why the work. The expands your horizon and will help you decipher some excellent insight that you can apply in future. Many a time, when you experiment, it also yields you good results and hence your opportunity set expands over time. You have very clearly outlined “why” it is worth undertaking such exercise. Thanks again for this wonderful write up!

I have come to realize that the most important factor to long term success is to understand which approach suits your temperament.I got it after 1 yr to 1 and half years of investing. Following that is also important like following value investing when one invest in value stocks.

Really interesting point. One company that I feel really fits in this example is Eicher motors. The brand has a phenomenal equity and I feel it will retain this competitive advantage for some time till some of the indian players develop products in its segment or a foreign player enters in a really big way. Currently the stock seems to be way overpriced but something I am definitely interested in. Few points working in its favor1. The motorcycle business is growing faster than CV business and is more profitable. This has been driving constant margin expansion2. With its waiting period due to high brand pull the business runs on negative working capital cycle. 3. ROCE numbers kind of indicate presence of a MOAT (brand has near monopoly in 150K + bike segment) which is likely to last for sometime atleast. 4. CV business though slowing down is still profitable and indications are of cycle turning. Definitely one to watch out in my list

hi dhwanilthanks for the comment. agree , being rigid limits ones learning and a lot of times the opportunities too. people like me have learnt this after a long time ..but better late than never :)rgdsrohit

Hi satya prakashtrue ..however in cases like me it has taken much longerrgdsrohit

hi neeravagree on eicher motors ..its worth studying. investing at current valuations is a different matter. personally I don't own itrgdsrohit

Hi Rohit,this is a well written and insightful post. Thanks for sharing.My five cents on the subect. Finding such great companies that deserve being expensive is a really tricky task. I mean just imagine going back in time when such a company was just getting by and ask yourself if the outcome of its decisions were in any way predictable. If not, you are probably seeing patterns in hindsight where there was only chaos in the moment.”I have never quite understood the point of these debates. There is obviously no single way of making money in the stock market. There are short term traders, buy and hold guys, debt specialists and all kinds of people in-between. Each approach has its strengths and weaknesses and no one can claim that a specific approach is inherently superior to the other, unless they are equally proficient in both.”That is a good point, and I totally agree. The only problem is that most investors haven't got a clue who they are as an investor. To what category they belong.I really think that most people would be better off, first sitting in a room alone, doing nothing and figuring out who they really are as an investor, i.e. getting to know themselve. And than start in the endavor of value investing.I recently have written a post on that subject on my blog, which could be of interest to you.http://undervaluedjapan.blogspot.de/2016/01/self-awareness-value-investing.htmlRegardsOtto

very informative & novel article