Bear markets are a good time to reflect !

In a bull market, any pick – good or bad, goes up and everyone feels like a genius. However at times like now, where any kind of mistake is brutally punished, it is easier to uncover flaws in one’s investing process.

So, I have been thinking about my investing process and have realized that one part of my process is exceedingly weak – The selling process

Why should one worry about the process ? If you are interested in understanding it in more detail – read this noteon ‘process versus outcome’. In a nut shell, if you get the investing process right, the outcome (investment returns) will take care of itself. It is the equivalent of getting your batting technique right, if you want to be a good batsmen and get high scores consistently.

As most of you are aware, I am heavily influenced by warren buffett and his investment philosophy. My introduction to investing was through his ‘shareholder letters’ and as a result, I have taken his teachings to the heart.

One of the key tenets of buffett’s philosophy is buy and hold, where one looks for companies with sustainable competitive advantage and buys them at a reasonable price. Once you make the purchase, buffett advises the investor to hold for long periods of time (provided the business maintains its competitive position)

The above is a very sensible approach and would work for majority of the investors. At the same time, the key point in the ‘Buy and hold’ philosophy is to buy a high quality company where the intrinsic value is growing and let time do its magic (via compounding).

A differentiated approach

It has become slowly dawned on me (I am slow learner J), that one needs a more nuanced approach to sell, depending on the nature of the investment. In the rest of this post and the next, I will try to categorize the various types and look at the sell approach one needs to adopt for each of them – This is ofcourse a work in progress and by no means any kind of rule set for me.

Such companies look cheap when the economy is doing well and expensive when things are bad, such as now. If you were to buy and hold such companies over the course of the entire economic cycle (from bottom to top to bottom), the overall returns would be very average. The key in such type of investments is to be able to buy when the company is at or near the bottom of the cycle (difficult to identify usually) and sell as the business recovers – without waiting for the cycle to top.

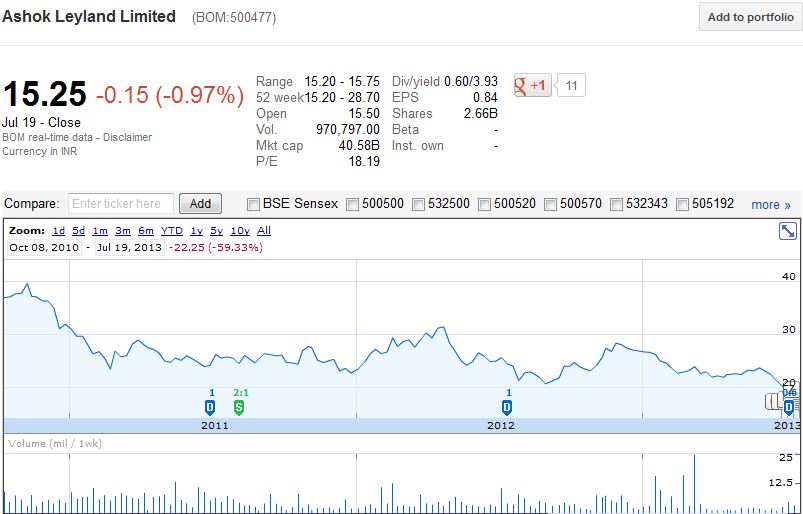

I wrote about the company herein 2008 and kept buying it as the stock crashed during the lehman crisis. My average cost basis was around 11 / share (post split). I was out of the stock by mid 2010. You can see the price action below

The commercial vehicle business turned in 2010 and has been going downhill since then. The stock price has followed suit

So the key point with cyclicals is this – Buy and hold does not work (usually) and timing is critical for above average returns

—————

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.

dear rohitu follow buffett, i follow u.but where was the durability of any competetive advantage in leyland. my take is that it always has been a commodity business and buffett insists much much more about the economics of the business than the underlying value. it should always be good business at fair value —egdabur, marico, gillette, 3m, pidilte, asian paints,and if at all u have faith in the management , stay with the stock or add in downturnsso, i still feel the flaw is still in the process

hi madhupvi disagree …Ashok leyland is not a commodity play ..cyclical yesIt has a modest competitive advantage esepcially in the south. truck drivers/ operaters dont buy a truck ..they care about the make and brand. the service network is importantthat said, its a cyclical stock. what i did not cover in the post is that there growth cyclical which grow over a full biz cycle and some cyclicals merely achieve the economy growth rate.so one can buy a growth cyclical and do well by holding, but returns are not as high as a franchise business like asian paints.in this case, ashok leyland was simply a valuation play in 2008. i bought it because it was dirt cheap.although buffett has advocated high quality stock, he used to invest a lot in these valuation plays in his earlier days.the point of my post is not to avoid such stocks, but to ensure you are sure what you are getting into and have the proper process for itrgdsrohit

Bang on target. It's easy to buy when everything is cheap but difficult to do the selective pruning so necessary for the good health of one's portfolio.I have been doing it albeit partially. That results into a bloated portfolio. Work in progress, as usual.

dear rohitthanx rohit. growth cyclical is very new to meand ur portfolio of 2008 containing asian paints, niit tech , balmer, gsk cons etc still provide with great returns. cyclicals may be for sophisticated investors like u .god bless

Hi Rohit,Have you ever analysed the company Hindustan Zinc? I wanted to get your expert advice on this one.I have been following and researching about this company for around 2 years and then decided to buy it.As per my analysis I found the stocks fair price to be around the 120/- level (after 50% margin of safety on IV). I started purchasing the stock from last year in small amounts and now hold a sizable amount of shares with average price of 110/-.However, I am not sure why this company's share is stagnating at such low levels. Some of the negatives that I could think of were:Zinc prices have hit rock bottom. It was slapped with rulings from court. It has put money on Cairns India, a business where it has no experience. Govt still holds a sizeable interest in the company. No idea when they are planning to divest.However this stock has been falling for last 2 years though it is consistently reporting higher FCF YoY.I would be really grateful if you could have a look into this one.Regards,Shantanu

Rohit,Buffett's BRK letters to shareholders is for ordinary investors who do not have much time for investment activities. For a 'professional' like you, one should read old Buffett Partnership letters and how Mohnish Pabrai copied it and using it successfully.

hi luckytrue ..best time to sell something which is not working out is immediately ..easier said than donergdsrohit

Hi dr madhupvyes, those companies are quite good and worth holding to. at the same time, i have had duds from time to time and it is important to clean those up and learn from themrgdsrohit

hi shantanui had a cursory look at hindustan zinc. it is facing the same issues as nmdc and other PSU- it is owned by government. market hates govt owned companies- it is generally high cash flows and keeping it on balance sheet. market thinks the goverment will just waste that money- general pessimismso fundamentally the company is dong ok..at the same time the above concerns are real – on what the govt will do with all the cash flow and how it will be invested.you need to answer these questions to make a long term these. as for me- i have very little faith the government will do anything sensiblergdsrohit

hi anoni have read buffett partnership letters and have followed mohnish for quite some time. at the same time, there is a lot to be learnt by every investor by reading the letters to shareholders too.one learns a lot on how to evaluate businesses by reading these lettersbtw..i am not a professional:) i do this part timergdsrohit

Hi Rohit,This is in response to your tweet,i am IT handicapped so do not have any tweeter handle or facebook..never saw you so negative toward india.I feel the these TRIO(chidu,montek,raghuram) will perform somesort of magic trick,to bring things on track……….but then we all stop believing in magic once we grow.RegardsAnurag Awasthi

hi anuragI am negative towards how things have been handled by the government. I feel very angry with them.that said, i invest bottoms up and never let my macro views influence my stock ideasregardsrohit