There are only a few times in the world of investing when you can be fairly sure. Most of my equity analysis has words like likely, could be etc. Equity investing is a probabilistic exercise. You can 60-70 or maybe 90% confident, but no one can say anything with a 100% confidence. There is no such thing as a sure gain.

There are only a few times in the world of investing when you can be fairly sure. Most of my equity analysis has words like likely, could be etc. Equity investing is a probabilistic exercise. You can 60-70 or maybe 90% confident, but no one can say anything with a 100% confidence. There is no such thing as a sure gain.

That is however not the case with the downside. Sometimes you can be sure that you will lose, no matter what. For ex: if you jump from the 4th floor of a building …you get my hint.

With stock markets down, the tendency of a lot of investors would be to take refuge in fixed income instruments such as Bonds, FD etc. But are they really safe ?

Inflation is now at 11.5% and it could stay there for some time. The usual policy action is to raise the short term to slowdown the growth and also the inflation. Due to the poorly developed debt markets in india, RBI does not have the same leverage as other central bankers in developed countries such as the FED. As a result, the RBI will have to raise the short terms rates pretty high to influence inflation. This was the case in the mid 90’s when the RBI had to raise the rates to around 13% to damp the inflation.

The current returns on Bank FD’s is around 10% for 1 year duration. Similary fixed income debt funds are providing a return of around 8-9% before expenses. Net of expenses the returns would be 7-8%. So if you decide to invest in a long dated FD be prepared to lose at least 2-3% of principal by way of inflation.

In the year 2000-2003, interest rates came down from 10%+ to around 7-8%. As a result debt funds gave 15%+ returns during that time period. We could see that phase in reverse now. As short term rates rise, debt funds could give negative returns.

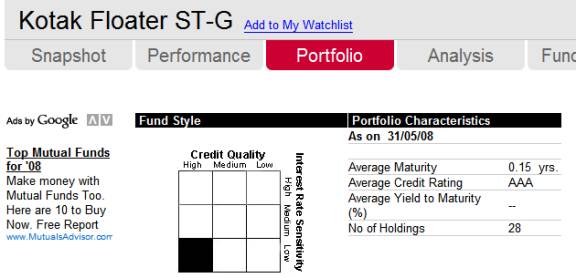

So what should one do ? If I have invest in fixed income debt, I would prefer short duration floating rate funds. See here , to understand what is duration.

I would generally look at the following points when selecting a short duration floating rate fund

– duration of the fund. Should be less than a year. See average maturity in the image at the top

– average credit rating should be AAA

– Known fund house

– Returns for the last 2-3 years should have atleast matched the category returns.

This is kind of investing is really a defensive one. The best outcome one can hope for is preservation of capital net of inflation.

That’s investor psychology for you. I think one can do a Phd on this. I’ve tried explaining the same logic to some friends and family members but every one seems to have a standard response as if they have all gotten together and decided to give me one reply ” 8 % is better than -ve”.

mahendra – in a way they are rational from their perspective. very few people are comfortable to invest in equity on faith where you may incur losses now and make good returns in a 2-3 years v/s a confirmed 8-9% on debt. some of us get that confidence because we have conciously worked at it.i however never advise anyone …money is generally too emotional a topic for most people

Mahendra, A bit off-topic here, but is this article in DnaMoney written by you? It’s not fair to blame fund managers http://www.dnaindia.com/report.asp?newsid=1176844—Manish

Rohit, Mahendra,I think mostly local investors are interested in short term returns and don’t really consider Post Inflation returns. People think stocks are like gambling..wich could be depending on how one invests.Such Blogs as Rohit’s..hopefully will educate investors.Vikas

mahendrainteresting to see you write for a publication. did not know you ran a mutual fund distributorship. vikas – i think only a very small % of people will change their mind. a lot of visitors to this blog (i think) are already following the valueinvesting approach and hence stumbled upon this blog.

Manish- The article is written by me.Rohit-Yes I have started MF distribution recently